Periodicity Decoupling Framework for Long-term Series Forecasting

{kind=link}

Abstract

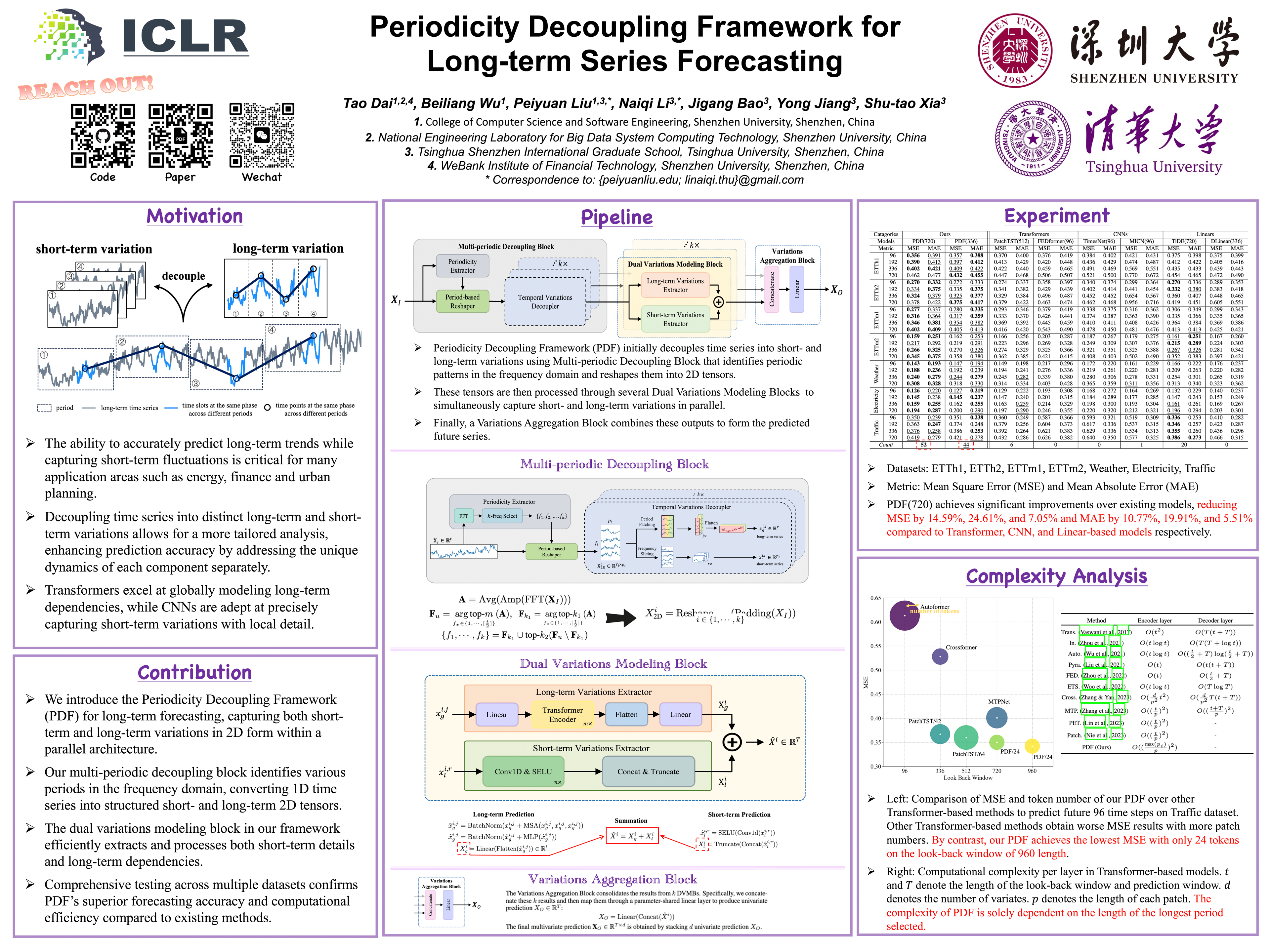

Convolutional neural network (CNN)-based and Transformer-based methods have recently made significant strides in time series forecasting, which excel at modeling local temporal variations or capturing long-term dependencies. However, real-world time series usually contain intricate temporal patterns, thus making it challenging for existing methods that mainly focus on temporal variations modeling from the 1D time series directly. Based on the intrinsic periodicity of time series, we propose a novel Periodicity Decoupling Framework (PDF) to capture 2D temporal variations of decoupled series for long-term series forecasting. Our PDF mainly consists of three components: multi-periodic decoupling block (MDB), dual variations modeling block (DVMB), and variations aggregation block (VAB). Unlike the previous methods that model 1D temporal variations, our PDF mainly models 2D temporal variations, decoupled from 1D time series by MDB. After that, DVMB attempts to further capture short-term and long-term variations, followed by VAB to make final predictions. Extensive experimental results across seven real-world long-term time series datasets demonstrate the superiority of our method over other state-of-the-art methods, in terms of both forecasting performance and computational efficiency. Code is available at https://github.com/Hank0626/PDF.