STABLE: Shift-Tolerant Allocation via Black-Litterman Using Conditional Diffusion Estimates

{kind=link}

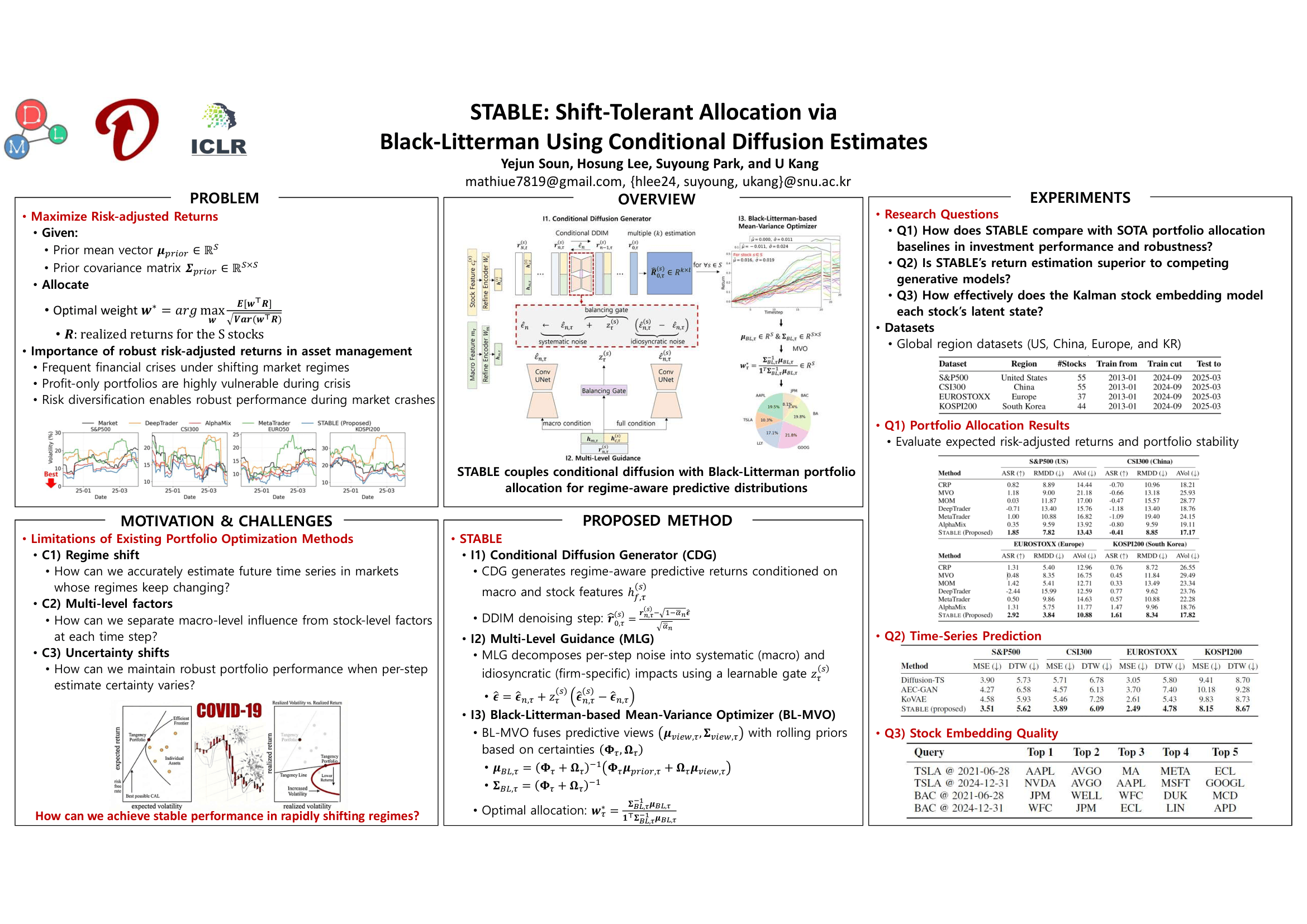

Abstract

In dynamic financial market characterized by shifting regimes, how can we make effective investment decisions under the changing 1) market regimes and 2) their impact? Among many research fields in financial AI, portfolio allocation stands out as one of the most practically significant areas. Consequently, numerous researchers and financial institutions continually seek approaches that improve the risk–reward trade-off and strive to apply them in real-world investment scenarios. However, achieving robust risk-adjusted performance is extremely challenging, because each asset's return and volatility fluctuate according to the shifting market regime. In response, modern portfolio theory (MPT) addresses this issue by solving for asset weights that maximize a risk–reward objective, using estimates of the return mean and covariance from historical returns. Reinforcement learning (RL) frameworks have been introduced to directly decide portfolio allocations by optimizing risk‑adjusted objectives using asset prices and macroeconomic indices. In this work, we propose STABLE (Shift-Tolerant Allocation with Black-Litterman Using Conditional Diffusion Estimates), which combines a diffusion-based generative model that captures regime shifts with an estimation-based portfolio allocation module that maximizes expected risk-adjusted return. STABLE takes macroeconomic context and asset-specific signals as inputs and generates per-stock return trajectories that reflect the prevailing macro regime while preserving firm-specific dynamics. This yields regime-aware predictive return distributions at the single-stock level together with a coherent covariance structure, which are then incorporated as investor views within a Black-Litterman allocation module to obtain risk-diversified portfolio weights. Empirically, STABLE delivers superior portfolio outcomes, achieving up to 122.9% higher Sharpe ratios with reduced drawdowns across major equity markets. It also attains state‑of‑the‑art time‑series estimation, lowering MSE by up to 15.7% compared with generative baselines.