GCGNet: Graph-Consistent Generative Network for Time Series Forecasting with Exogenous Variables

{kind=link}

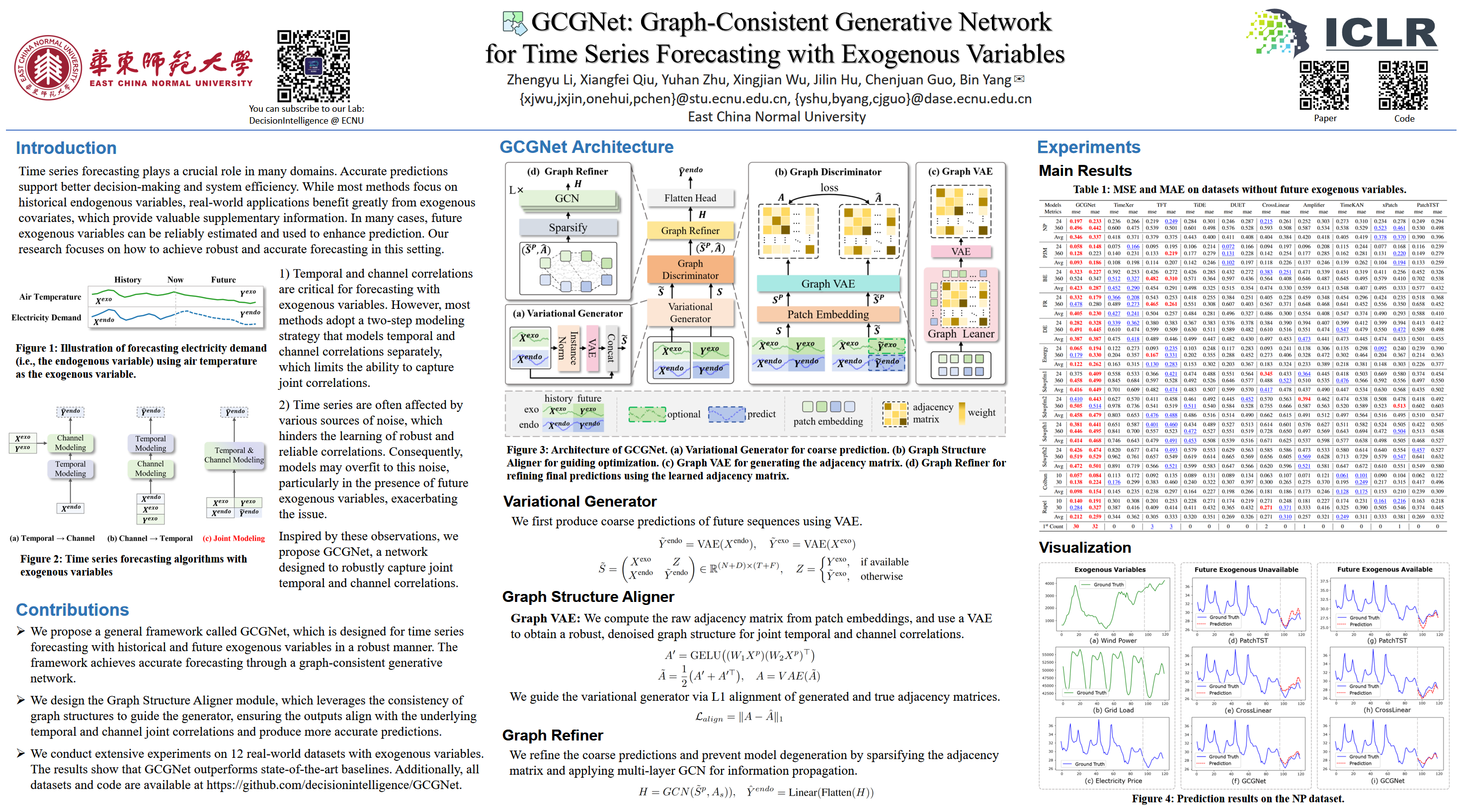

Abstract

Exogenous variables offer valuable supplementary information for predicting future endogenous variables. Forecasting with exogenous variables needs to consider both past-to-future dependencies (i.e., temporal correlations) and the influence of exogenous variables on endogenous variables (i.e., channel correlations). This is pivotal when future exogenous variables are available, because they may directly affect the future endogenous variables. Many methods have been proposed for time series forecasting with exogenous variables, focusing on modeling temporal and channel correlations. However, most of them use a two-step strategy, modeling temporal and channel correlations separately, which limits their ability to capture joint correlations across time and channels. Furthermore, in real-world scenarios, recorded time series are frequently affected by various forms of noises, underscoring the critical importance of robustness in such correlations modeling. To address these limitations, we propose GCGNet, a Graph-Consistent Generative Network for time series forecasting with exogenous variables. Specifically, GCGNet first employs a Variational Generator to produce coarse predictions. A Graph Structure Aligner then further guides it by evaluating the consistency between the generated and true correlations, where the correlations are represented as graphs, and are robust to noises. Finally, a Graph Refiner is proposed to refine the predictions to prevent degeneration and improve accuracy. Extensive experiments on 12 real-world datasets demonstrate that GCGNet outperforms state-of-the-art baselines.