Option Market Making via Reinforcement Learning

Zhou Fang ⋅ Haiqing Xu

{kind=link}

Abstract

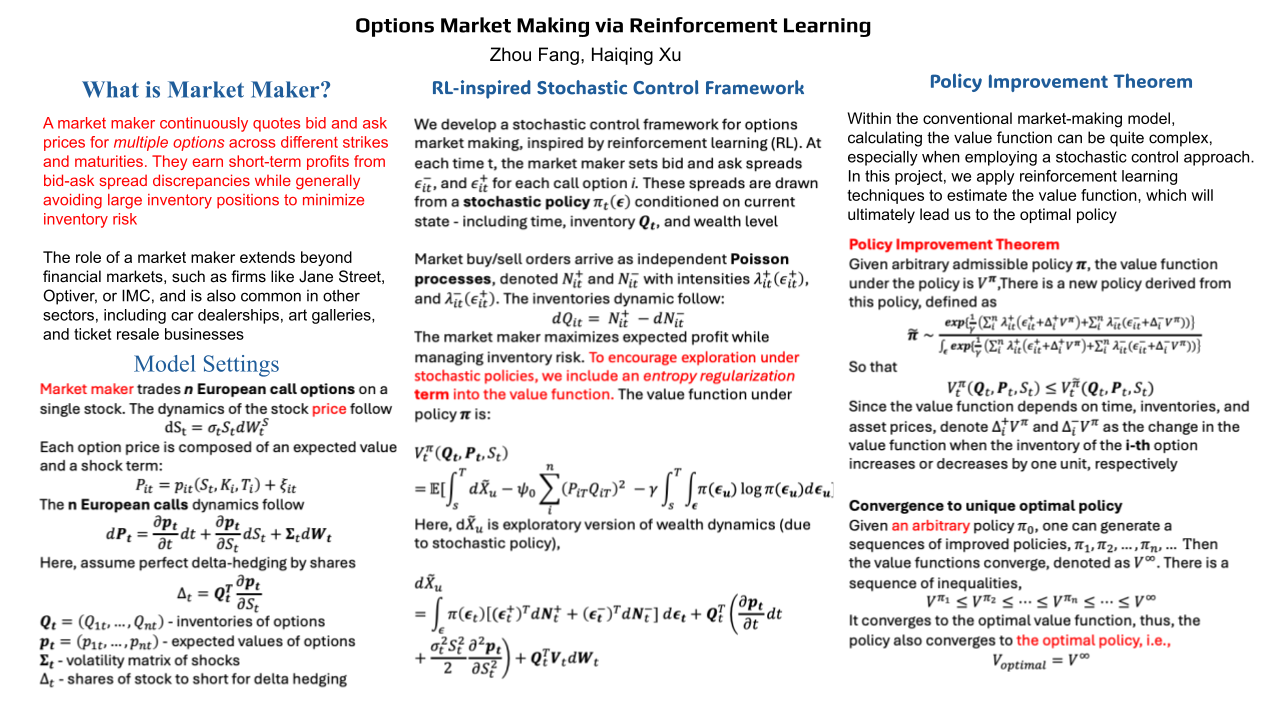

Market making of options with different maturities and strikes is a challenging problem due to its highly dimensional nature. In this paper, we propose a novel approach that combines a stochastic policy and reinforcement learning-inspired techniques to determine the optimal policy for posting bid-ask spreads for an options market maker who trades options with different maturities and strikes.

Chat is not available.

Successful Page Load